Last week we launched our comprehensive 2016 SBA and USDA Loan Market Outlook. At 20 pages, we know this is a lot to digest — so we’ll summarize the key takeaways here, starting with our intent.

Why read a 20-page SBA and USDA lending outlook?

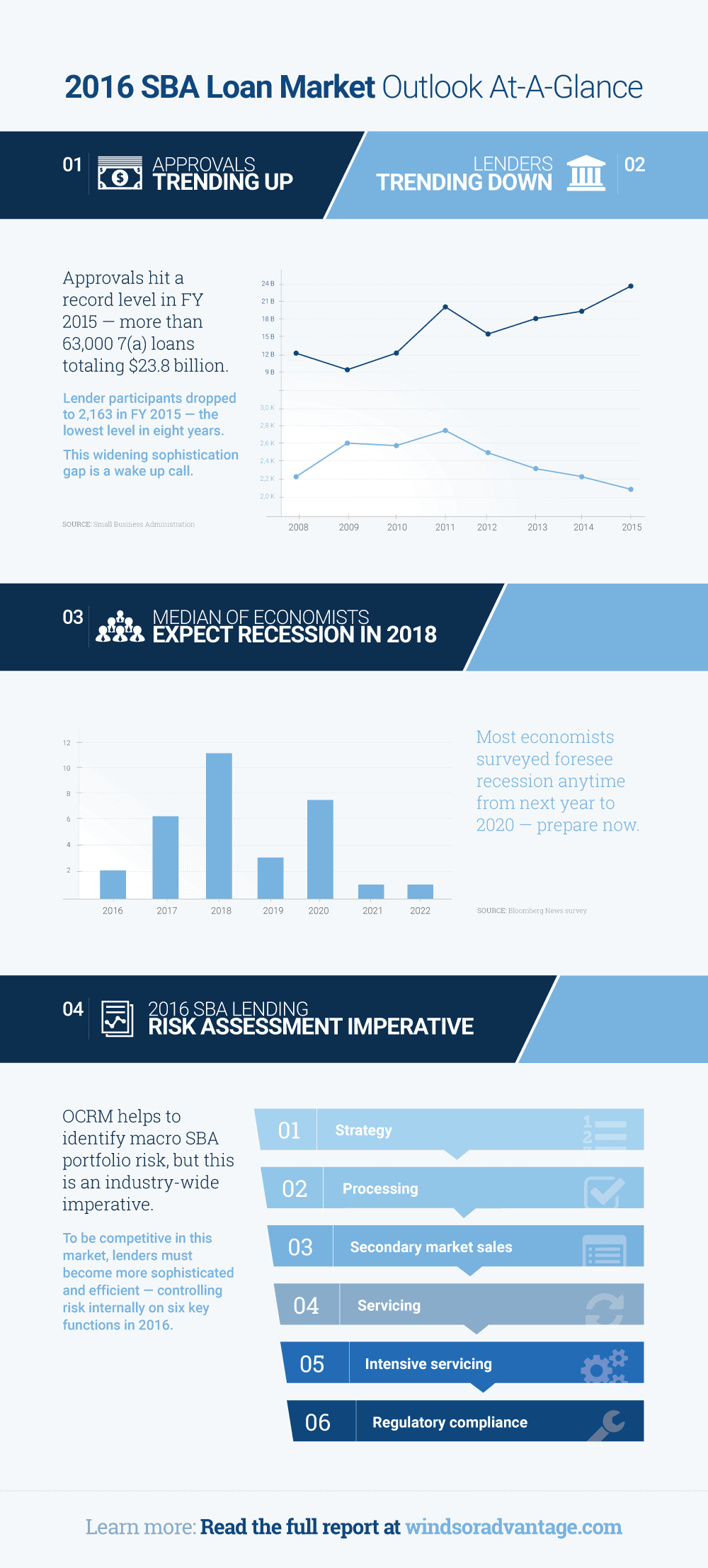

The day-to-day conversations we have with lender clients often focus on pressing tactical issues like the eligibility of a prospective borrower or a payment modification for an existing borrower. But to ensure that we provide the most effective guidance to our clients, we need to step back and look at the big picture of SBA and USDA lending on a regular basis. As the first chart in the following infographic shows, this is not a static market — and the year is already off to a volatile start. Doomsayers are once again banging their “recession is looming” drums. Statistically, they are going to be proven right sooner or later. Likely sooner.

We view it as our responsibility to report on trends we see unfolding and present a proactive framework that can be used to advance the risk management of every SBA and USDA lender — whether they are a client of ours or not. We hope that you take the time to read our inaugural outlook — or at least scan it for the most pressing issues — and consider the implications for your SBA and USDA lending business. Our team gathered the best data available at the time of publication to forecast key market dynamics. Candid constructive criticism is invited and encouraged, as we will refine our outlook on an ongoing basis.

Four key 2016 SBA outlook themes summarized

No time to read our outlook? Along with the infographic below, we’ll summarize the four key themes we believe define the SBA and USDA lending market in 2016:

- SBA and USDA loan approvals at a record high. SBA approvals hit a record level in FY 2015 — with more than 63,000 7(a) loans totaling $23.8 billion. This 23% increase in the total dollar volume of loans represents the third consecutive year of growth in the financing of businesses through the 7(a) program. While some of the increasing volume trend may be due to economic growth and SBA and USDA program changes, much of this sustained increase in volume is more likely due to the increasing sophistication of SBA and USDA lenders. So let’s focus on that.

- Lender participants at the lowest level in eight years. The number of lender participants in the 7(a) loan program continues to trend down — dropping from a highpoint of 2,728 in FY 2011 to 2,163 in FY 2015 — the lowest level in eight years. The top 50 lenders by volume provided more than half of all SBA 7(a) and USDA loans in the last fiscal year. Sophisticated, competitive lenders are driving a widening gap — fewer and fewer participants are funding more loans than ever.

- Recession expected in the next five years. We just witnessed the worst start to a year on record for the U.S. stock market. After nearly seven years of economic expansion, doomsayers are increasingly vocal about a looming recession. Tuning out the pundits, we still think these are useful reminders to prepare your SBA business for the next downturn by assessing and refining controls and processes. The median of 31 economists in a recent Bloomberg survey now expect a recession in just two years, and most of the economists foresee a recession anytime from next year to 2020. Recessions are notoriously difficult to predict, but we must prepare for them nonetheless.

- The imperative for better risk controls. Recessions tend to impact small business borrowers disproportionately. Small businesses are often forced to close within months during an economic downturn. To be competitive in this market, all lenders must become more sophisticated and efficient. The SBA’s and USDA Office of Credit Risk Management (OCRM) will help to identify inherent risk in the macro SBA and USDA portfolio — but all market participants should analyze and control risk internally as well. Risk assessment and compliance should be managed through consistent controls within all SBA and USDA lending processes. But in 2016, the highest functional priorities are most likely strategy, processing, secondary market sales, servicing, intensive servicing and regulatory compliance.

Whether you use this framework or your own, we encourage all SBA and USDA lenders to make risk assessment a top priority for 2016 and discuss these topics with their SBA and USDA lending advisers.

Please contact us if you have any questions about this post or the 2016 SBA and USDA Loan Market Outlook.