We recently explored some of the most important items to consider when using an SBA loan to help grow your small-business in The Pros and Cons of SBA 7(a) Loans. Although SBA loans may require time and effort, the long-term advantages outweigh the cons for many small-business owners. Specifically, those owners interested in longer repayment periods and lower interest rates.

If you’ve made the decision to pursue SBA financing, the application process can seem intimidating in the beginning. However, keeping these four main areas top-of-mind can help you efficiently and effectively navigate the process from start-to-finish.

1. Identify Loan Purpose

Be specific. Lenders need to understand why you’re in need of financing, how much money is required and how you intend to use the funds. You should be able to articulate how the loan will help your business, how it fits within your overall growth strategy and accurately forecast projections based on the desired loan amount. Not only do lenders appreciate business owners who can effectively convey this messaging, but it will also help expedite the pre-approval and underwriting processes. Keep in mind some of the following examples when updating your business plan:

- Refinance existing debt

- Purchase equipment or inventory

- Acquire a business

Be sure to have a detailed explanation prepared for other business expansion opportunities (i.e. hiring new employees, advertising or marketing, opening new locations, etc.).

2. Understand Eligibility Requirements

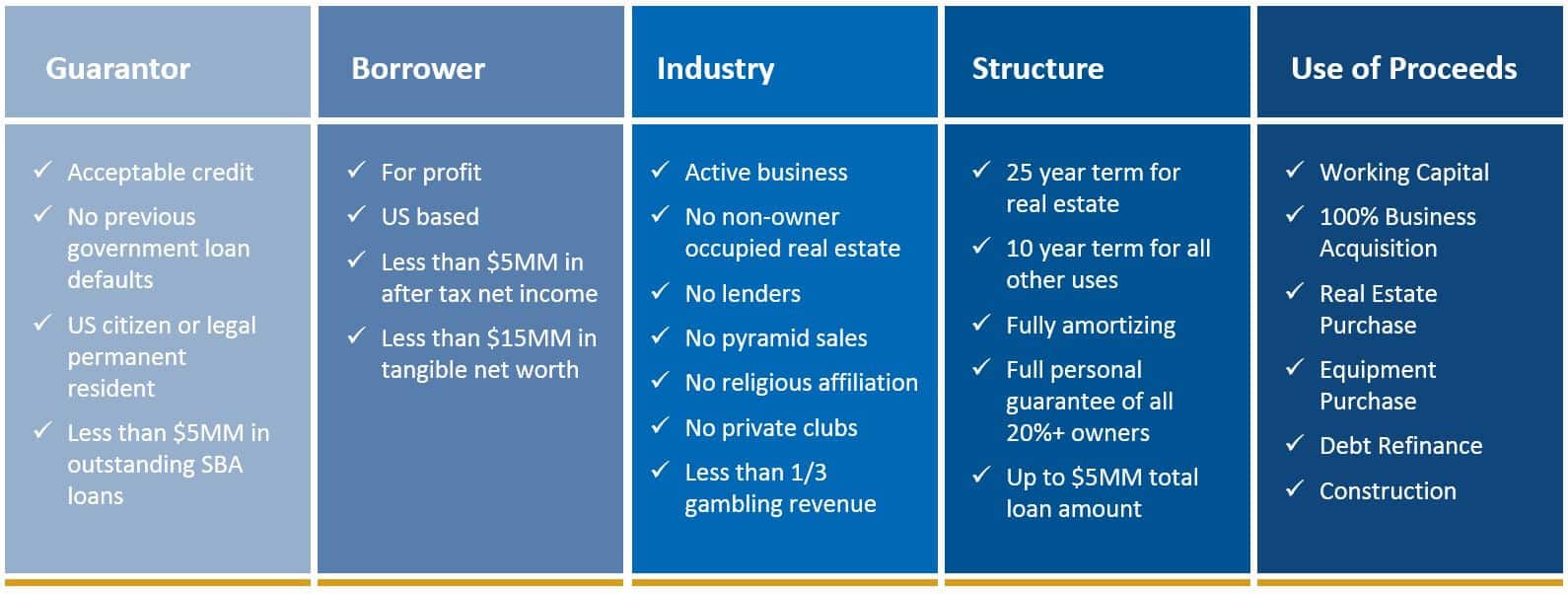

The SBA has specific eligibility criteria for businesses, guarantors and uses of proceeds and an applicant should understand these criteria. SBA 7(a) loan applications can be time consuming so it’s critical to ensure certain eligibility criteria is met prior to investing significant time and effort. Eligibility for the SBA program can be summarized across five general categories:

Many SBA lenders will have their own unique set of eligibility requirements over and above SBA guidance. Personal credit score, how long you’ve been in business and cash flow considerations are typically included in a lender’s determination for approval. Many, but not all, SBA lenders require the following:

- Operating business for at least 2 years

- Minimum personal credit score of 650

- Minimum global DSCR of 1.25x

Mitigating considerations that may allow for an SBA loan include personal liquidity and prior industry experience.

3. Prepare Your Documents

Once you’ve identified a need for capital, how that capital will be used and have determined a basic understanding of the qualification requirements, it’s time to start gathering your documents. The SBA 7(a) loan application process requires specific documentation, regardless of which financial institution makes the loan. While the entire documentation package depends on the nature of the transaction and the lender, the initial request will include:

- Business and personal tax returns (past three years)

- Business debt schedule

- Business interim financial statements

- Personal financial statement for all guarantors

This initial request will be followed by additional documentation for items including legal documentation, leases and other documents necessary to document and close the loan.

4. Find the Right Partners

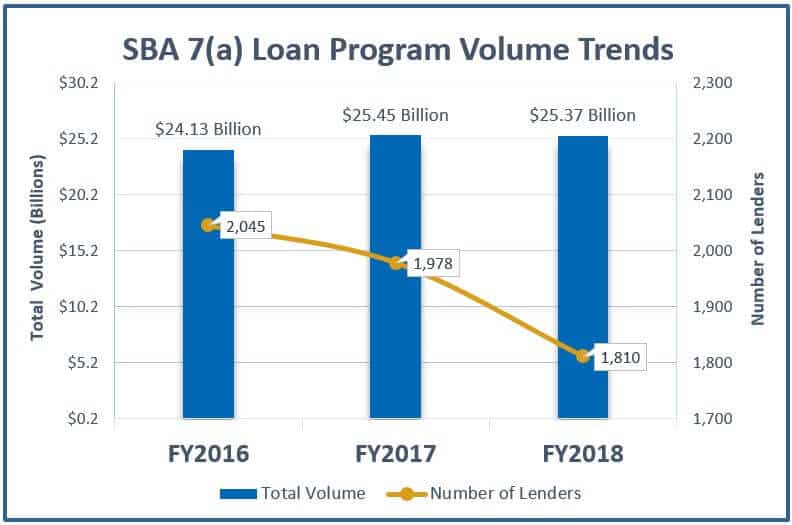

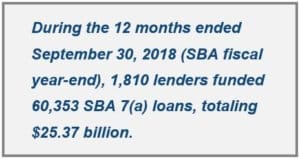

Many financial institutions offer various types of SBA loans, ranging from small community banks and credit unions to large national banks. Last year, 1,810 different lenders in the U.S. approved at least one SBA 7(a) loan application.

“Preferred” SBA lenders have the capacity to expedite pre-approvals while non-delegated lenders are required to submit a complete application package to the SBA for approval. In addition, the emergence of online SBA marketplaces has allowed small-business owners to obtain funding in as quickly as 10 days from submission. When researching partners, it’s important to consider:

- Type of Lender – You can get small-business loans from several institution types that may specialize in certain products, including banks, credit unions, CDFI’s (Community Development Financial Institutions) and online lenders

- Delegated v. Non-Delegated – Experienced SBA lenders can apply for “delegated” authority which allows the institution to expedite the approval process

- Online SBA Loan Marketplaces – Service providers that do not fund loans but rather assist with connecting potential borrowers to experienced lenders through the utilization of streamlined processes and technology

- Other Resources – Your local SBA District Office and/or local SBDC (Small Business Development Center) can help provide free or low-cost consultation

Putting together a complete SBA loan application is no easy task but the benefits clearly make the effort worth it. The lender will want to uncover a significant amount of information about your business to determine credit worthiness. To be successful, you must stay organized, highlight the positives about your business in the loan application and be extremely responsive when asked for additional information. The speed of the pre-approval and underwriting processes will ultimately depend on the information you’re able to provide. If you’re on top of things, you can put your best foot forward and obtain funding quickly.

About Windsor Advantage, LLC

Windsor Advantage provides banks, credit unions and CDFIs with a comprehensive outsourced SBA 7(a) and USDA lending platform.

Since 2010, Windsor has processed more than $2.3 billion in government guaranteed loans and currently services a portfolio in excess of $1.3 billion (as of May 31, 2019) for over 85 lenders nationwide. With more than 150 years of cumulative SBA and USDA lending experience, cutting edge technology, rigid controls and consistent processes, Windsor is uniquely qualified to assist any size lender with implementing a thoughtful and profitable government guaranteed lending initiative.

Windsor Advantage has a team of 30 professionals with offices in Chicago, Illinois; Indianapolis, Indiana; Seattle, Washington and Charleston, South Carolina.