This article is excerpted from The 2022 Mid-Year Lending Report, our annual forecast of key market dynamics based on the best data available at the time of publication. Download your copy to access the full report of SBA insights from experienced industry leaders.

SBA 7(a) Secondary Market Outlook

Secondary market conditions are unlike anything we’ve seen in the last 20 years, excluding the 2008 financial crisis. Premium prices for available inventory right now hover just under 110. At this same time last year, premiums were averaging closer to 120. Increased SBA activity, rising prepayment speeds, and an influx of guarantees on the secondary market have driven down demand and, consequently, prices. Lenders should prepare to exercise patience and potentially reevaluate their Sell/ Hold strategies to cope with the current cycle.

Despite its current downturn, we expect the secondary market will continue to be a strong fee income driver for financial institutions that adjust their strategy accordingly.

Current Conditions

Premium prices have dropped below where they typically run in a normal market for the first time in eight straight years. The ultimate question the secondary market faces: can demand keep up with supply this year?

Supply

Record volumes of loans are on the secondary market right now. In 2008, the market size for guarantees reached $3-4 billion. It’s more than doubled since then. A historic $1.7 billion in guarantees were available at the end of May 2022. This trajectory puts us on track to reach $2 billion in available pulls just over halfway through the calendar year, 20% of last year’s entire SBA issuance.

Lenders should expect to see some collapse in pricing once the market value surpasses $1B. It comes as no surprise that premiums have dropped dramatically this year.

Despite lower premiums, lenders continue to report healthy pipelines to the secondary market and inventories continue to grow. This volume was fueled by economic conditions during the pandemic, low-interest rates for borrowers, an increasingly widespread access to government-guaranteed financing. Coupled with additional lenders entering the space, conditions were primed for extraordinary growth. Even deteriorating premium prices have not deterred the rising volumes of supply on the secondary market which will continue to suppress premiums.

Demand

Demand has struggled to keep pace. All asset classes experienced significant changes in the first and second quarter of the fiscal year, SBA premiums included. Mortgage rates went from sub 3% to 6% in a little over 6 months. Investors have seen portfolios drop in value by approximately 10%, levels that usually take a couple of years to achieve.

SBA guarantees on the secondary market are not immune. If anything, the industry’s tie to the Prime rate rather than a market rate causes it to lag the curve without the same hope for quick recovery. Where other asset classes can act more responsively, the SBA industry is dependent on a Prime rate that only adjusts quarterly. Pricing cannot recover as quickly, but it can certainly disintegrate because of other market

behaviors, namely, prepayment speeds.

Constant Prepayment Rate (CPR) is the measure of loan prepayments as a percentage of the current outstanding loan balance and is the key indicator for tracking the performance of SBA 7(a) pools. As of the end of Q2 2022, pre-payment rates are up at least 50% year over year. In 2021, the CPR was 8% and borrowers were still receiving payments from the CARES Act. The CPR is now 12%, and it doesn’t seem to be slowing down. If we maintain the trajectory established in the first half of 2022, there is a very good chance we could end this year with a 14% CPR base case. For context, this would be a 75% increase in prepays compared to 2021.

2022 SBA Secondary Market Premiums

SBA 7(a) loan premium data is not widely published. This often makes it difficult for many lenders to ensure they are getting the highest secondary market premium, even in normal markets much less in those marked by uncertainty.

To be more competitive in the current market, lenders should prepare bid sheets and submit the opportunity to no less than eight investors. Only through experience can lenders gain current knowledge of the most active investors and the highest premiums based on the structure of each loan.

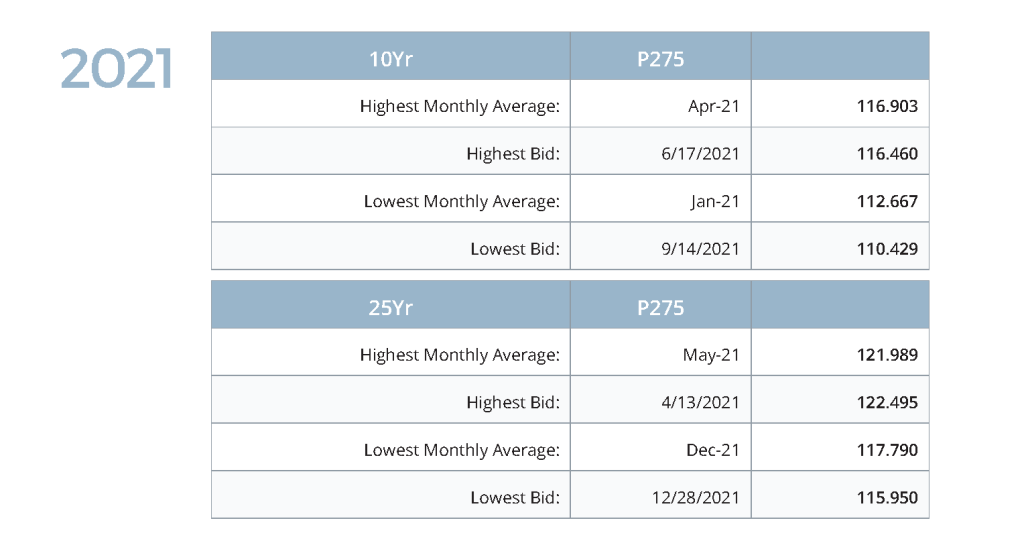

The need for quality, guaranteed, variable-rate assets will continue to bolster the 7(a) and USDA secondary markets, regardless of pre-payment speeds. Based on a sample of more than $250 million in government guarantees sold through Windsor’s platform last calendar year in 2021, the table below shows SBA Secondary Market Premiums on 25-year loans were as high as 121. 99 and bids on 10-year loans were as high as 116.46.

Compare those numbers to Q1 and Q2 Secondary Market Premiums for the calendar year of 2022.

Economic Corrections Impacting the Secondary Market

Lenders must remember that we’re examining outlier trends as we analyze the recent secondary market data. Keep in mind our Q1 and Q2 2022 data compares the beginning of a bear market against the peak of last year’s historic bull run. Trends in this industry are cyclical just as the rest of the economy.

The secondary market performed exceptionally well throughout 2020-2021. Those who joined the SBA space in recent years only experienced an unusually strong market until premiums started dropping in September 2021. Comparatively, this year’s changes in premiums seem further pronounced.

The continuous downward trend in premiums we’ve experienced since is uncharacteristic of even a normal market. Compared to recent success, this turn has fueled market pessimism that continues to widen the gap between supply and demand, however, change may be on the horizon as economic conditions adjust to the impending bear market and base rates continue to rise.

Much of the pessimism clouding the secondary market outlook stems from overarching economic uncertainty. Demand is reliant on many external factors that are out of lenders’ control, however, some relief may be in sight. Rates increased again at the end of July 2022 by another 75bps. Additional increases to the Prime rate should begin to temper some of the excess supply on the secondary market and stabilize demand.

Conversely, as rates rise the cost of borrowing grows more expensive. As a result, prepayment speeds could continue increasing to keep demand from rising back to more stable prices.

The key takeaway here is to stay patient. Like other markets, the secondary market for guarantees will not correct itself overnight. Apply short-term strategies to cope with current challenges but keep a long-term mindset as you build your strategy

for the secondary market.

Lender-controlled Factors to Consider

While lenders cannot fix the overarching problems weakening demand in the secondary market, they can adjust their strategy to accommodate expected market corrections. Patience will be crucial. You may also want to reconsider current Sell/Hold Strategies as a short-term solution to tide over your institution for the long run.

If you choose to hold, make sure you discuss with someone who can anticipate how the market will react to those maturities compared to shorter ones. It may influence your strategy on maximizing the cost-benefit of SBA lending as a fee income driver at your institution.

The following lender-controlled factors should be considered when structuring loans and estimating potential premiums:

- Time – 10-year loans should be bid to the secondary market immediately upon full disbursement and at a maximum, within thirty (30) days of funding in order to garner the highest secondary market premium. 25-Year loans should be bid within the first ninety (90) days.

- Term – Longer terms receive higher premiums. 25-year terms result in a higher premium than 10-year terms.

- Spread – Maximum spread over prime is 2.75% on loans over $50,000. Maximum spreads receive the highest premium.

- Adjust – Quarterly and monthly adjusts receive the highest premiums, versus annual adjust and fixed rate loans.

- Size – Lenders should expect that every $500,000 of a guaranteed portion above $1,000,000, premium will drop by roughly a quarter point (0.25%).

Download the Full Report for SBA Lenders.